Have you been thinking about how you could survive being old and out of work? Even without a job, you’d still need to buy necessities, pay the mortgage, insurance, home, and car maintenance, and more. With all these bills that need to be paid for, you’d need an additional source of income as long as possible.

As you may know, there is a policy of having income from funds you’ve reserved within an insurance company. These funds can have returns that can last for a lifetime that can cover your basic necessities.

This method performed during the 18th century has specified a group of presbyterian ministers. Almost two centuries later, having lifetime payments has been implemented to the common American population.

Now, the income-generating policy that people have been familiar with for over 300 years now is called an annuity. Learn more about annuity as a whole, ordinary annuity, and annuity due through this article.

What is an Annuity?

An annuity is a type of policy that insurance companies or financial agencies offer. This can have your funds last through a lifetime, referred to as insurance for retirement. You can have these scheduled for receiving with your agent. It lets you have the regular income immediately or years later. You can also buy an annuity policy one-time or by a series of payments once agreed upon.

There are many kinds, types, and variations of annuity that can match your liking.

An annuity has two types with reference to the exact schedule of payment within a specific period. These two types are called ordinary annuity and annuity due.

Ordinary Annuity

This type of annuity is called ordinary because most deals happen in his type.

Definition

Ordinary annuities are best for payment transactions. You can easily tell the type of annuity you are encountering once you’ve seen it. Here are some signs of Ordinary annuity as it has the following characteristics:

- All payments have the same amount. (Example: A series is to be paid at $500 every paying period)

- All payments are executed at the end of each period. (Example: Payments are due on the last days of a month.)

- The payments that occur in an ordinary annuity are made in the same intervals. (Example: weekly, monthly, semi-annual, or yearly schedule of payments.)

To further incorporate this knowledge, here are some examples that ordinary annuity is being made that you might not even notice:

- Bond payments made semi-annually

- Dividend payments due quarterly or yearly

- Employer’s pension payments given every month

- Car loan payments due at the end of a covered period

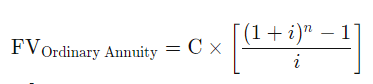

How to calculate an Ordinary Annuity’s Future Value?

A future value entails the value of your money at a certain point. Knowing how much your money would be in the future can be determined through two methods of computations.

What you need to know the future value (FV):

- 1. Amount of regular payment or the cash flow per period (C)

- Number of intervals of payments (n)

- Interest rate (i)

For example, you will calculate the Future Value of your monthly investment of $1,000 per month. By having a 5% interest to be made at the end of each month for five months, you can calculate by two methods:

Method 1

Multiplying 105% to the monthly investment with an exponent of zero for the first month. Then, multiply with an exponent of one on the second, and so on, until the fourth exponent on the fifth month. Once computed separately, add the results together, and the answer would be $ 5,525.64.

Method 2

You can also obtain the future value of your investment with the equation below and have the same results to $ 5,525.64.

Source: Investopedia

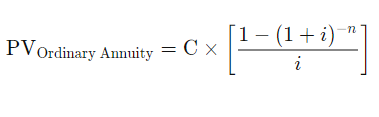

How to calculate an Ordinary Annuity’s Present Value?

You might also aim to have a specific amount of money in the future. If this is the case, you can also calculate how much you need to attain the desired amount of monthly payment. The details below can show how you get a present value of an ordinary annuity using two methods:

What you need to know the present value (PV):

- Amount of regular payment or the cash flow per period (C)

- Number of intervals of payments (n)

- Interest rate (i)

Using the example above, having a 5% interest rate for five months with monthly due of $1,000, the present value would be:

Method 1

Get the amount of cash for payment divided by the interest rate to the power of 1 on the first month, the second power on the second, and so on. The answer will result in $ 4,329.48. Knowing this would get you an idea of how much you need to have those 1,000-dollar payments.

Method 2

An easier method would be having to calculate using this formula:

Source: Investopedia

This solution will give off the same answer as the first method amounting to $ 4,329.48.

Annuity Due

Annuity due is the opposite of ordinary annuity in some aspects but has a greater amount of present value.

Definition

You might want to know if a specific payment is an example of an annuity due. This type of annuity is appropriate for receipts. As some important payments fall into this category, check off this list of its characteristics to confirm:

- Like an ordinary annuity, annuity due is also a series of payments made at the same interval.

- All payments are due at the start of each covered period.

A few common examples of this type of annuity is as follows:

- Rental or lease payments are made every cycle beginning.

- Payments for insurance premiums.

How to calculate an Annuity Due’s Future Value?

It’s given as an example of knowing the annuity due’s future value to a rental payment. You can calculate as required through the following:

What you need to know the future value (FV):

- C = Cash flows per period

- i = interest rate

- n = number of payments

Having these variables, use the formula:

Source: Investopedia

To check your computation, follow this example:

Suppose the assumed interest rate is 3% in payment due to every beginning of the month, amounting to $1,000 for ten months. In that case, you can calculate the annuity due’s future value by following the formula above. This computation would result in a total of $ 11,807.80.

How to calculate an Annuity Due’s Present Value?

The present value of your annuity due would indicate the current value of the payments to be made in the future. This computation can show you if you should receive a series of cash payments or lump sum, like winning a lottery.

Source: Investopedia

What you need to know the present value (PV):

- C = Cash flows per period

- i = interest rate

- n = number of payments

Using the same example for the future value of annuity due, you would get $8,786.11.

Ordinary Annuity and Annuity Due – which is better?

Which annuity is better can be defined if you are a payee or the payer. If you are the payee, it would be more beneficial to take on the annuity due. This way, you could use the value of your payment immediately.

Most payers, on the other hand, prefer the ordinary annuity. This preference is because you can use the resources worth your money before you pay.

Ordinary Annuity and Annuity Due: The Key Differences

Even if these two are of the same kind, the key differences between the two stand out. In summary, here are a few points where ordinary annuity and annuity due vary from each other:

- Payment in Ordinary annuity is the end of the period, while for annuity due, it is for the succeeding dates.

- The present value of annuity due is higher than the ordinary annuity.

- The amount of annuity due is smaller than ordinary annuity as it includes interest per period.

- An ordinary annuity is preferred to someone who makes payments and annuity due for those who receive payments.

The Stages of Annuity

The two stages of annuity are the accumulation and distribution once you have put in your funds to grow over time.

Accumulation

Accumulation is the phase wherein the funds are being put into an account and grown.

Distribution

The distribution phase involves giving out funds while you are alive. Once the distribution has been started, you cannot revoke the decision again.

Keep in mind that the annuity expires. When this happens, you cannot make any more payments, and no duties are obligated to be fulfilled by each party. If you die, you can pass on the funds to your official beneficiaries.

Takeaway

One of the main advantages of annuities is to provide a constant source of income for a long time. And choosing the right annuity can depend on which lifestyle and financial situation you are currently in.

To personally compute your fund value can determine which is more beneficial for you and your payment application. If you are planning on more comfortable days of retirement, having annuities is strongly preferred. This way, you can generate income and enjoy it when you’re old. This will be all while not having a job anymore and being debt-free

Check out these articles that might also pique your interest:

- How To Use A Life Insurance Policy To Be Debt-Free: A Long Term Solution

- What It Means To Be Bonded, Licensed & Insured?

- Should You Get Life Insurance? A Breakdown Of What It Is

Want to know more? Let me know through your comments below!