What’s the classic American dream as we see it in those old black and white movies?

Hard work and sacrifice, all translated to having a good job, a good home, and a good family. It still holds true to a lot of people today.

Being able to have their dream house is a major life milestone and may possibly be the biggest financial transaction of their lives. While it all sounds well and lovely, buying a house can actually be pretty complex.

A big reason for that is that the system that manages these transactions are actually pretty outdated and takes a very long time to accomplish.

Today, I will talk to you about a rising star in the fintech industry that has changed the game for traditional mortgage lending: from shortening the waiting time of three weeks to just a couple of minutes, to lowering annual percentage rates and stacking costs in the long run.

What is Better Mortgage?

Better Mortgage, or Better.com, comes from the new breed of digital mortgage lenders with 24/7 online assistance and on-demand human assistance. All services and paperwork involving buying a new house, from pre-approval to loan application, can now be accomplished without having to be physically present.

It’s pretty easy too– you can learn the entire home-buying process by yourself on Better.com’s website, and it also has a YouTube channel to explain mortgage concepts to boot. There’s also a separate app for mobile, as well as an online tracker for your application process.

Also read: What is a mortgage?: all you need to understand about it in 2020

Kinds of Mortgages Offered

Better.com offers five mortgage loans:

1. Adjustable-rate mortgage

After an initial fixed period, the annual percentage rate of this type of mortgage varies. Better.com has three offers: 5, 7 and 10 years fixed-rate, and 1 year for how often the rate will increase or decrease after the fixed-rate years.

This is best for homebuyers that are looking at more short-term plans that want to resell it after some time.

2. Fixed-rate mortgage

Better.com has 15, 20 and 30-year fixed-rate mortgages, which basically means that the interest rate will remain the same throughout the entire loan duration. This is best to get if you’ve permanently decided to own the home for the long-term.

Learn more about the differences between fixed-rate and adjustable-rate mortgages here:

3. Refinance

Refinance is for homeowners that are paying off any existing previous mortgages and looking to secure a new loan. Better.com charges only closing costs and no origination fees.

4. Conventional loans

Conventional loans are determined by which county the home actually is. Better.com offers jumbo loans if you’re interested in buying a home that’s above the purchase limit of that specific county.

5. FHA loans

FHA loans remove the burden of the huge down payment, only requiring the 3% minimum. This way it allows potential customers with a more precarious credit history to apply for loans with a 15 or 30-year fixed-rate loan.

Fees and Rates

Better.com’s edge over the majority of its competitors is that it doesn’t charge any additional fees that usually come with the traditional mortgage rates. The 24/7 customer service is provided by loan officers over the phone and doesn’t operate on commission, making them neutral advisors and not salespeople looking to make you pay more than you’ve intended.

| FEES CHARGED | Appraisal fees | These are fees made based on an estimated value of the property being purchased. It ensures the buyer that the value of the home is enough to cover the loan. |

| Title Insurance fees | A form of indemnity insurance for the holder in case of any defects in a title to a home that may result in financial loss. | |

| Credit report fees | This covers the cost of obtaining a copy of and reviewing your credit scores. | |

| FEES NOT CHARGED | Lender fees | These are charged by banks for processing and funding a loan. They may or may not be separated from application fees and underwriting fees. |

| Loan officer commission fees | Loan officers are “commissioned” by charging you fees (often called settlement costs or processing fees) throughout the processing of your loan or in ways hidden throughout the whole application, such as charging higher interest rates. | |

| Application fees | Traditional mortgage lenders usually charge multiple application fees upon purchase. They can also be doubled if you’re paying less than the standard 20% down payment. | |

| Underwriting fees | These are fees charged by the mortgage lender for preparing the loan and the paperwork. |

Before you proceed, here’s a quick refresher on the kinds of mortgage fees

Pros and Cons

Best Features

1. Low mortgage rates

Because it accepts FICO credit scores that are generally lower than what most lenders would accept, Better.com charges lower mortgage rates compared to major rates when it comes to 30-year fixed-rate mortgages.

When it comes to 30-year durations, having a substantially lower mortgage rate will matter if you add up everything you’ll be paying in a year.

2. Easily accessible online

Because everything is accessible online, it removes all the fees associated with every step of the process and paperwork charged by traditional mortgage lenders.

The cost of buying a mortgage is immediately cut down to the one you’re actually applying for, and in a way that’s very convenient to everybody.

Here’s Vish Garg, the CEO, and co-founder of Better.com, on what online mortgage lending can do:

3. Faster mortgage pre-approval and closing time

Better.com’s best feature is its three-minute pre-approval time. A verified pre-approval is guaranteed to still be faster than the traditional way, taking only 24 hours.

Drawbacks

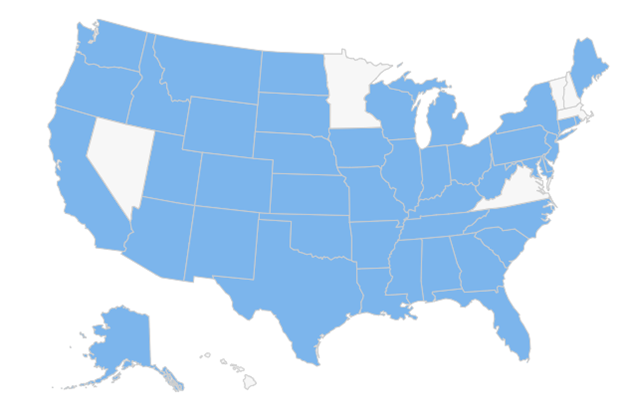

1. Not licensed in all states

Better.com is licensed in only 36 states, so there’s a huge chunk of target audience that can’t access its services.

2. Missing out on other loan types

Since Better.com offers only five loan types, it may miss out on potential clients looking for other types like:

- Construction projects: Also known as a “self-build loan”, construction project loans are short-term and used to finance the construction of homes and real-estate projects. They usually have higher interest rates because of the added risk.

- Mixed-use properties: These combine private money loans, commercial loans, government-backed and construction loans. This type of loan is used by any buildings with at least two zoning units.

- Co-op mortgage: This type of loan lets you purchase shares in cooperative housing, where the corporation retains the actual ownership of the property while potential residents purchase shares that will let them stay in parts of the property.

- Manufactured homes: Manufactured homes are separate purchases from the land it sits on and has different types of loans: personal property loan, chattel mortgage loan, etc.

- Multi-family homes or buildings with five or more units: These range from duplexes to apartment buildings with more than a hundred units. The best you can get for these is an FHA loan but that only covers up to four units.

How do I qualify for Better.com?

1. Must be from a licensed state

Better.com is accessible in the following areas: Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, Washington D.C., Florida, Georgia, Idaho, Illinois, Iowa, Indiana, Kansas, Kentucky, Louisiana, Maine, Maryland, Michigan, Mississippi, Missouri, Montana, Nebraska, New Jersey, New Mexico, New York, North Carolina, North Dakota, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Washington, West Virginia, Wisconsin, and Wyoming.

2. At least 620 FICO credit score

Better.com requires that you have at least 620 as your credit which, if we’re being honest, is lower than most mortgage lenders would be willing to entertain. FICO credit scores range from 300 to 800, and 580 is generally considered fair.

Still, it won’t hurt to improve your credit scores a bit before applying for any kind of mortgage, so you can get better rates and save more money.

3. Employment history and income

Better.com scrutinizes your financial status overall, which can get a little complicated if your verified income is separate from what you receive from overtime and commissions.

Self-employment can get pretty tricky too. Mortgage lenders have to be confident that you can pay all of the mortgage payments for the whole loan duration, which usually goes from 15 to 30 years, depending on what it is.

For the down payment (20% of the home price), Better.com looks at your current savings.

4. Debt-to-income ratio of up to 55%

Your debt-to-income ratio is the monthly debt that you pay depending on your lifestyle (credit card debts, car payments, loans, etc.) compared to your monthly income.

How do I get a mortgage with Better.com?

The site already immediately presents four options: pre-approval (basic or verified), refinance, and mortgage application. The entire process is pretty quick compared to traditional lenders, with an estimate of how long it will take you to complete each step.

You will need to create an account to upload all your financial details for Better.com’s soft credit check.

For the pre-approval process, Better.com will scrutinize your credit score and history, bank statements, income, and overall financial capability. The entire process takes three minutes.

Once you’re pre-approved, you will receive a basic approval letter which will tell you the loan products you’re qualified for, as well as the estimated monthly payment and annual percentage rate. Everything is personalized according to your financial history.

Better.com then assigns a permanent servicer to handle the loan payments for the remaining term. However, if realtors need something more concrete, then you’ll need a verified pre-approval letter.

This means having to upload more financial documents, including W-2s and paystubs. It will take around roughly 24 hours to review the details and generate the pre-approval letter.

After that, Better.com will let you choose your preferred loan type from the four offers as well as the interest rate. To guarantee the interest rate of your choice, you’ll have to complete the entire application within the time frame Better.com required you to.

Relevant: Read here how you can avoid paying for Mortgage insurance

Better Mortgage FAQs

1. Does Better Mortgage pay private mortgage insurance?

On conventional loans with less than 20% down payment, yes. It may also charge FHA loans that always need mortgage insurance.

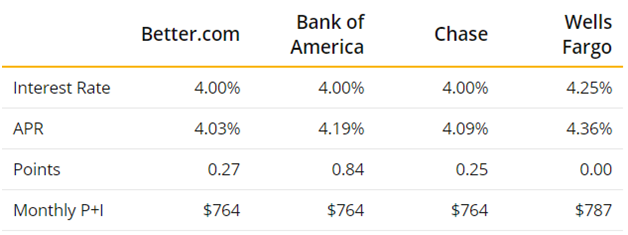

2. How does Better.com’s rates compare to other competitors?

Other than the application process being made extremely convenient, the rates are a huge plus too if you compare it to traditional offline lenders: the Bank of America, Chase and Wells Fargo are three popular first-option banks that base rates on a 30-year mortgage.

As you can see in the table above, Better.com has slightly lower rates that can actually be a big help to consumers.

The slight difference in numbers may not seem much, but if you think long term and how the costs are eventually going to add up, you’re actually going to be saving a lot more money especially if you didn’t have to pay origination fees as well.

3. If Better.com does not charge any lender fees, how does it make money?

Better.com makes its money from “end-investors”, who buy and sell mortgages on the secondary mortgage market, making their profit from the interest paid on home loans.

Bottom Line

My takeaway from the whole Better.com Mortgage experience is that convenience goes a long way in improving the efficiency of the homebuying process, going as far as removing all the fees placed on the bureaucratic traditional system.

Getting acquainted with the fintech industry is always a good idea, and going with Better.com is an even better one. But that of course depends on the kind of mortgage you’re applying for.

Bottom line, you won’t have to go through the painstakingly long process while being able to save more money than if you’re applying to other popular banks.

If you don’t find Better.com Mortgage to be the best mortgage lender for you, get started on looking around by using the same criteria: convenience and rates.

Like this article? Check out these articles on homeowners insurance:

- Understanding insurance premium deductible

- Know all about Insurance Umbrella policies

- Review of Lemonade insurance

Let me know in the comments below what topics would you like me to cover in the next posts. You can also follow me on Facebook here!