Student loans are a big part of how our society functions.

They are a sort of “necessary evil” with which we have new generations of well-educated young people even besides the fact that education can be quite expensive.

According to Forbes, in 2020 the student loan debt reached $1.56 trillion. This money is borrowed by 45 million people, and it is the second-highest consumer debt behind mortgage debt.

But, it is also the reason why many people are able to get the education that they need, and then make our societies better in return.

That is why choosing the right type of policies with the best options is imperative for everybody. In this direction, there are many companies out there that offer private student loans.

Many people know Discover as the company that is among the top banks that issue credit cards.

And they don’t stop there, they are offering many other financial products and services among which are student loans for different types of studies.

The amount of money you can borrow depends on the program that you choose. In some cases, you can borrow the full cost of attendance.

In this post, I will be reviewing Discover student loans, what are they offering, how are the prices moving, what are the advantages and disadvantages, and more.

According to this information, you can make an informed decision when it comes to choosing the right type of student loan for your educational needs.

Who can take a Discover Student Loan and how to apply?

The Discover Student loans are an excellent option for people that have scholarships, maximized grants, or other types of free financial aid and need a lender to support them.

The specific requirements for the loans are different depending on the type of loan that you need.

The process of applying for Discover Student Loan is extremely easy and simple. Once you did all your research and decided on all the important things, visit the Discover web page to apply.

You can apply from your computer, smartphone, another smart device, or even call them on 1-800-STUDENT.

Relevant: Read the review of Ameriprise insurance here

Types of loans and requirements

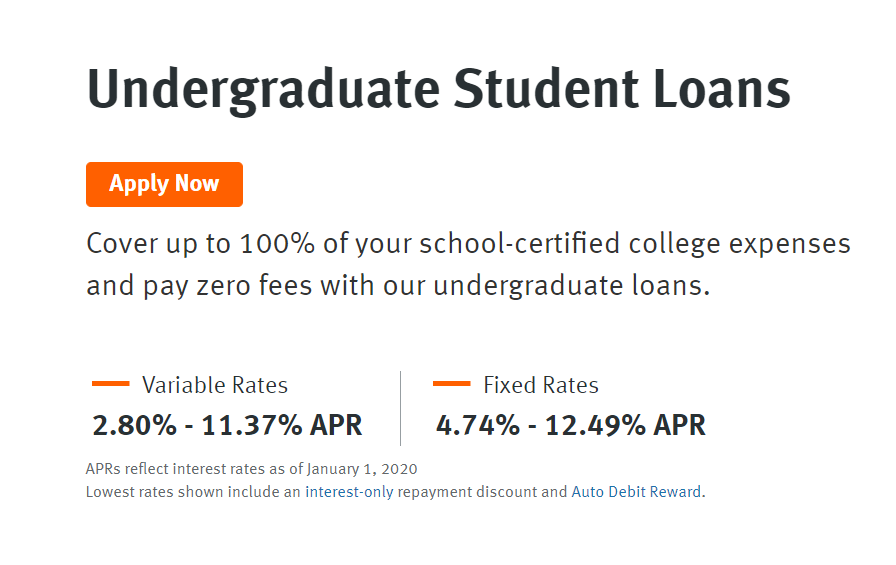

1. Undergraduate Loans

Using the Undergraduate Loan you can cover up to 100% of the school-certified costs in an eligible school that you choose for a Bachelor’s or Associate’s degree.

This type of loan is a good option for those of you who need just a bit more than their federal loans offer.

The good thing is that you don’t need to pay anything while you are finishing the undergraduate degree and there is also a grace period of 6 months after you finish.

However, if you feel like you should lessen your debt for when you’re finished, you can pay $25 per month while you are finishing the degree.

Another positive thing about the loan, as with all Discover loans, is that there are no fees and you don’t need to have a co-signer if you have great credit.

The repayment term is 15 years and that is longer than the Federal standard plan, but there are other options out there that offer longer terms also.

Now these types of loans sound good and they can be helpful for certain people, but you should try to avoid them and pay for the degree with a combination of federal loans, scholarships, savings, and even working.

Leave private loans as the last option.

2. Graduate Loans

Discover offers loans for graduate programs as well. The loans cover Law School, Health Professional Schools, MBA programs, and the traditional graduate or PhD programs.

In these types of loans you can again cover up to 100% of the costs of the program.

The Graduate loans operate just like the undergraduate ones, with some small changes.

Undergraduate loans have a grace period of 6 months as I previously mentioned, and the Graduate loans have a longer grace period of 9 months after graduating.

The option to pay $25 per month while you are in school is again up to your wishes and possibilities.

These loans sometimes require a cosigner, and in the cases where they don’t, you would need to have strong credit scores and history of education.

The repayment plan can be up to 20 years, which is a very good option for some people out there.

This type of loan is a pretty big obligation and you need to think about it. If you are finishing a graduate program that is likely to be highly paid, or necessary in the current situation then this loan makes sense for you.

A kind of “rule of a thumb” here is to not get a bigger loan than you’re expected to earn in your first year of employment after you graduate.

People who have a credit history with Discover and can qualify for better interest rates and no cosigners are in the best position here.

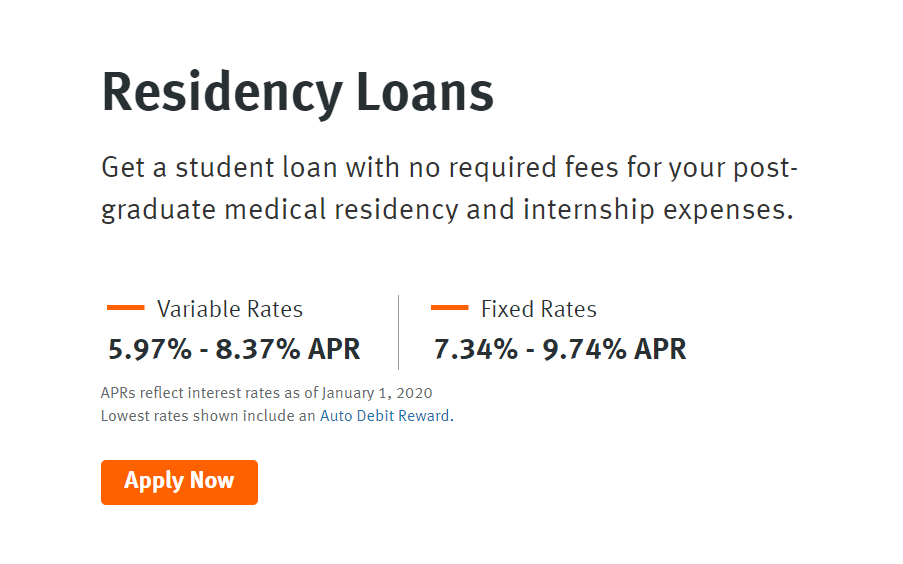

3. Residency Loans

After finishing medical school, many people want to continue into residency programs which are in most cases paying the doctors.

However, there are additional expenses like moving costs, housing costs, and very often people in residency programs start a family during residency and have more expenses.

In this case, you can take a Residency loan which will cover the costs of the residency, internship, moving, and board exam.

When it comes to the loan limits in this category they can be different according to the type of residency you choose.

Usually, the limits are higher for things like Dentistry, Pharmacy, Podiatry, Veterinary Medicine, etc.

And it is lower for Nursing, Physical therapy, Physician assistants, etc.

These types of loans can be done without cosigners in cases when you have an established credit history.

In all other cases, a cosigner is needed for the loan.

All in all, residency loans should be avoided as much as you can, but if you have no other option and your expenses are quite high, then Discovery loans are a good option after 0% APR credit cards.

4. Bar Exam Loans

Law students that need financial support for passing their bar exam can try the Discover Bar Exam loan.

The limit on this loan is $16.000 and current law school students are eligible for getting it.

The grace period on this loan is just as the Graduate loan or 6 months after you graduate. In case you have already graduated, you have to start repaying immediately.

No cosigner is needed if you have a credit history with Discovery, but many of the others will likely need a cosigner.

The repayment term on this loan is 20 years.

In practice, only the lucky ones get a job with a firm that is paying them a salary in the time they are studying for the Bar Exam.

The reality is that many law school graduates need the Bar Exam for getting a good job that will cover their expenses.

This is where if cutting the unnecessary costs doesn’t work, this type of loan can.

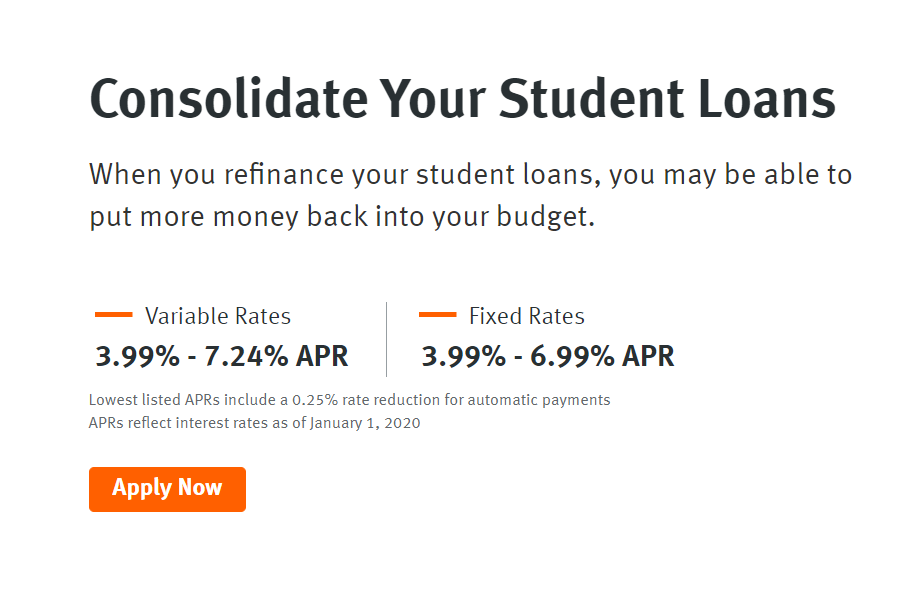

5. Consolidation Loans

Consolidation loans refer to refinancing and allow students to refinance Federal loans, or/and your already existing private loans.

The positive thing is that Discover loans have no fees, so it will be good for the students that choose these types of loans.

You might be required to have a cosigner, but this depends on the situation.

The minimum debt that you have to have is $5000, and not above $150.000 for being eligible for this type of loan.

The repayment terms can be either 10 or 20 years, and this will define the interest rates.

Consolidation loans are good for people that have previous student debt and they got a good, steady job with a decent salary.

Other types of loans that Discover offers to students are:

- MBA Student Loans: you can cover up to 100% of the college costs which are school-certified.

- Health professional loans: also can cover up to 100% of the total school-certified costs

- Law School loans: loans for law school that can cover up the whole sum of the school-certified costs

Advantages and Disadvantages of Discover Student Loans

As some of the advantages of these student loans I will list:

- You can get financial help easy and fast: you can easily apply for these loans through a very simple process on their website or through the phone. You can also ask anything that’s not clear to you

- There are no fees required: this means that during the process of applying for the loan, the origination, or at any other times no fees will be posed upon you.

- You can get rewards for good grades: Discover can give you a one-time cash reward on each loan in case you have a 3.0 GPA or some equivalent of that. The amount of the reward is 1% of the loan amount in cash.

- You can choose from different repayment options: you can make interest-only monthly payments while you are in school, you can give fixed $25 monthly payments, or you can choose the deferred option which has a grace period. Additionally, you can make payments anytime you want or have more money on hand to reduce your debts.

- You can get small loans: if you need just a bit of a push, you can get small loans that are easily returned. The lowest amount is $1000.

When it comes to disadvantages, I believe the following things are worth mentioning:

- In order to see if you will qualify and what rate you will get, you have to get a hard credit check

- Prequalification is not possible

- You have one option for repayment term, 15-20 years. The longer you borrow, the higher the interest you pay.

- No cosigner release option. This means that in a few years when you are stable, you won’t be able to release the cosigner from their obligations.

Conclusion

To sum it up, Discover Student Loans can be the right solution for your financial difficulties.

The loans can start from very low amounts, and you can choose one of the three repayment options which is extremely good for people that have an uncertain professional future.

Another great thing is that if you get your hands on some bigger amount of money, you can go ahead and pay it back, lowering your loan.

However, loans are a serious thing and they should be the absolutely last resort. Especially when it comes to students.

Student’s future is quite uncertain, and finding a good job in these times can be quite difficult and require some effort.

But in the end, investing in your education can never be too wrong. Education is the base of a successful professional career, and it can kick start your life for the better.

Consider the advantages and disadvantages carefully, and ask the right questions before you make a decision.

If you found this post helpful, you should check out some other reviews I have written in the past:

- How insurance companies generate revenue?

- Understanding medical insurance deductible

- How you can use life insurance policy to be debt free

Let me know in the comments below if you would like to read reviews of any specific insurance companies or services.